Three Primary Investment Objectives

We believe that there are only three investment objectives capable of being achieved and, so, worthy of pursuit:

- Staying out of irretrievable trouble — which is usually to be accomplished by owning high-quality securities and being broadly diversified.

- Participating in the markets or market sectors appropriate to the individual’s investment time horizon and personal tolerance for risk and volatility.

- Accomplishing the foregoing in as efficient a manner as possible in terms of minimizing taxes and not paying for services which add little or no incremental value to the investment process.

High Quality & Diversification

High quality and diversification in an investment portfolio serve a purpose similar to that of fire insurance on a house. We carry fire insurance not because we “expect” our house to burn down. We carry it because if we do not have it and our house does burn down, we may not be able to recover financially from the catastrophe.

Similarly, “high-quality” and “diversification” serve the purpose of “insurance” in an investment portfolio. They provide some degree of protection against an economic, monetary, or market calamity which we cannot foresee and do not expect, and which we might not otherwise withstand, or from which we might not otherwise recover without the added protection should such a calamity come to pass.

Risk versus Volatility

It is useful to draw a distinction between “risk” and “volatility” in the securities markets. If “risk” is defined as the possibility of experiencing a decline in the value of one’s investments from which one cannot recover, it should probably be minimized for most people. If “volatility” is defined as the normal fluctuations to which all securities markets are subject, it must be endured, if the rewards bestowed by those markets are to be enjoyed.

Time Horizon

For most people, the time horizon for their investment portfolio planning probably should be longer than they initially think. The attainment of retirement age is hardly a logical point at which to modify one’s investment policy. At the very least, one should plan for a period covering one’s life expectancy, and married couples should plan for a period covering their joint life expectancy. The life expectancy of an individual age 65 is 21 years, and the life expectancy of the second to die of a couple, each age 65, is 26 years. If one expects to bequeath a portfolio to one’s children and hopes that they will pass it on to subsequent generations, the time horizon for investment planning, for all practical purposes, becomes infinite.

Investment objectives are meaningfully expressed only in terms of investment time horizon and tolerance for risk and volatility, and not in terms of desired return. Everybody desires a maximum return but should expect to earn no more than what the markets in which they are invested bestow.

Stocks

We feel that investment in common stocks can be justified if the individual believes that there is at least a 50 percent chance that the money so invested will not be withdrawn for other purposes over the subsequent 5 years. Historically, the probability of such an investor’s realizing a positive return on his money over this investment time horizon, with even a randomly selected, unmanaged list of stocks, has approached 90 percent.(1)

Market Timing

We participate in markets; we do not try to outguess them. Market timing is a futile activity. The most successful investors, over time, are usually those who remain 100 percent invested at all times.

The evidence is overwhelming and incontrovertible that even the highest paid professionals are unable to predict with an accuracy of better than 50 percent such factors as short-term moves in the market, onsets of recessions or recoveries, changes in the direction of interest rates or foreign exchange rates, or changes in the rates of inflation. Therefore, such considerations should remain irrelevant to both the formulation of an investment strategy and the timing of investments or disinvestments. One should put money in the market when one has it to put there and withdraw it from the market when one wants to use it for something else. There should be no other timing considerations.

Because, for all practical purposes, the securities markets are efficient. The concept of employing a “professional money manager” to try to time the markets, rotate from market to market or sector to sector, or to buy individual securities when they are undervalued and to sell them when they are overpriced, is an exercise in futility. In this sense, there are no such “professional” money managers and so paying for such a service is counterproductive, serving only to reduce one’s overall total return.

Investing for Total Return

Except in cases where prohibited by law (as with certain trusts where income beneficiaries’ and remaindermen’s interests conflict), investors should utilize the “total return” concept of investing. This means that for investment selection, performance evaluation, and spending purposes, we believe they should draw little distinction between income derived from interest and dividends and income derived from growth of principal.

Market Returns

The best estimates anybody can make about future rates of inflation and future rates of total return are simple extrapolations of past long-term rates of inflation and long-term rates of total return. In this regard, the best historical measures we have cover the 81-year period from 1926 through 2006 and are as follows: inflation, 3.0 percent; cash, 3.7 percent; U.S. Government bonds, 5.4 percent; corporate bonds, 5.9 percent; large capitalization common stocks, 10.4 percent; and small capitalization common stocks, 12.7 percent.(2)

The differences between historical rates of return among the various asset classes are not random events. They are based upon a fundamental principle of capitalism that, for the system to attract investment capital, the greater the uncertainty of the timing of one’s rewards, the greater must be the magnitude of those rewards. The most successful investors usually maintain broadly diversified portfolios of the common stocks of high-quality, growth-oriented companies in unregulated (non-utility) industries.(3)

Security Selection

A good investment is one that represents the simple direct ownership of manmade, value-added, productive resources (plant, equipment, organization, patents, copyrights, trademarks, franchises, and human talent) as opposed to claims on mere commodities (precious metals, the commodities futures markets) or artificially created and/or leveraged risks (derivative securities such as common stock and interest rate options).(4)

If and when possible, it is far more efficient to own securities outright, rather than through the medium of either a mutual fund or a closed-end investment company. Though we may need to pay to buy or sell a security, we should not need to pay to own or hold that security.

Above-average current yields on investments are indicators of less desirable investments. High current yields usually indicate low quality and a likelihood that the current yield is unsustainable, a low likelihood of any significant improvement in future performance, or both.

Mutual Funds

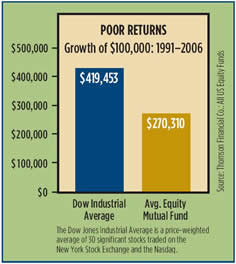

Over the 20 years ending in 2006, the average owner of equity mutual funds earned 2.42 percent less per year than the average shareholder invested directly in a randomly selected and unmanaged list of U.S. stocks. For the average owner of a mutual fund invested in U.S. Treasury bonds, the shortfall over the past 20 years, relative to a randomly selected, unmanaged list of U.S. Treasury bonds, has been 2.26 percent per year. For the average owner of a mutual fund invested in foreign stocks, relative to the U.S. stock market, the sacrifice has been 3.67 percent per year over the past 20 years. For the average owner of a mutual fund invested in foreign bonds, relative to U.S. Treasury bonds, the sacrifice has been 1.93 percent per year over the past 20 years.(5)